How To Create Your Own "Sequence" Of Investing

(Investing Sequence)

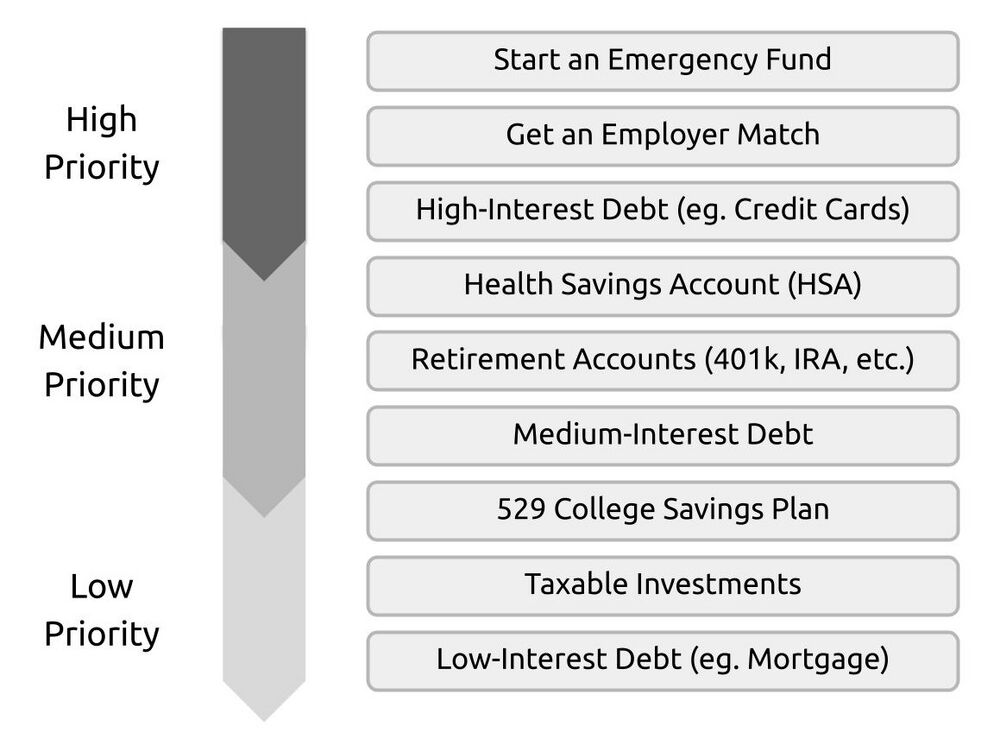

(Investing Sequence)

Choosing what to invest in is hard, here's how to make it easy

The first thing you need to understand about money is that it's like energy and actually most of what wealthy people use it for is to go make more money. They use the money they have today to try to find efficient ways to go buy more future money. This is called investing. Sending money to go try to duplicate itself…what an interesting game. Why does money matter so much to everyone?

In the early stages, most people think money is simply a tool to buy things they want or to survive with. In the olden days, we had bartering, now we just trade silly paper (digitally) because that's the easiest.

But in reality, for the economy in total, money is a tool that is being leveraged to get people to do things in the world! It's like stored economic energy. It's what creates a lot of action.

Now the reason I gave this little background is because it's vitally important to understand WHERE YOU ARE in the money game right now. By understanding your current position, you can invest in the right bucket to ensure your money is being used as efficiently as possible.

What are the buckets of investing?

Okay so there are a million ways to cut it, but here are my personal buckets:

-

Active Income This is income derived from your current work, energy, skills, & labor.

-

Longterm Investments These are taking care of your "end game", retirement, family, late-life medical stuff, and setting yourself up to grow old and ride into the sunset with comfort. It's the easy, safe, smart moves.

-

Asymmetric Opportunities These are when you find something with MASSIVE upside potential and relatively low risk. They are usually rare, one-off opportunities that come about only when you have your ears tuned to the right frequency. You find these as you go through life based on your personal knowledge and skills.

-

Passive Income This is when you simply get recurring money being produced from assets and you don't do any work. It's what everyone dreams about but is mostly fictitious until you have a LOT of money or owned assets.

I'll explain why and how I think about each bucket and when to invest in them. But notice, I will never tell you what to invest in because I don't know your situation, I don't know the right answers, I have no clue why we are even here on this planet, and I could be completely wrong about everything I'm about to write… but here's how I choose which bucket to invest in.

My first rule of thumb is very simple. If I'm not able to save and invest 50% of my income, then I will keep my focus on MAKING money and learning new skills until my margin gives me a wiggle room of at least 50% of my income being disposable to invest with. This could mean reducing living expenses in some cases, but I'm particularly focused on just making more money first. This number may be different for everyone, but this gives me room to take a little more risk and feel comfortable with it.

If you don't have the extra money to invest with, you shouldn't be focused on investing! you're wasting your time on the WRONG stuff. Spending time investing is a low-leverage activity when you don't earn that much. You need to earn money first. Invest in your skills first. Develop yourself first.

Basically, the whole point of this entire article is to examine how to spend time & money where you have the most leverage. For people early in the game, that starts with controlling your earning potential.

Here is the sequence & how to use it:

- ACTIVE: focus on active income first, and invest in your skills while you're young, this increases earning potential and allows you to earn more than your time is worth. Skills compound the same way money does, but you need skills first! This means buying courses, knowledge, mentorship. Also, your skills/knowledge is what will allow you to later find asymmetric opportunities that others can't. This is always your foundation + fallback. You CANNOT skip this step.

Stay in this bucket until you can stash away at least 6k per year for a Roth IRA.

- LONGTERM: While investing in your Active Income and back into skills, simultaneously stash away ~6k per year for a Roth IRA. This way your long long-term retirement is taken care of, tax-free, and you're always "on track". If you aren't earning enough to stash away 6k per year, go back to step 1. I also would include your emergency fund in this “long-term” bucket, which is a 3-12 month savings fun in case anything happens.

After the Roth IRA is taken care of, keep investing back into your skills & active income until you're at that 50% margin we talked about.

- ASYMMETRIC: Reverse engineer your goals. Want to be financially free by 40? Need $X to do that?

You will need to invest in riskier bets that could pay off and make you wealthy while you’re young. High reward with the lowest risk. The way you find these opportunities is by finding a knowledge gap or skill gap that you can exploit in a market (something you're particularly good at or interested in). It may appear risky to others, but you have an edge on it & feel confident putting big skin in the game. This is NOT diversification time. I said to have a 50% margin so you could feel comfortable taking a risk here. If you're extremely risk-averse, you may opt to skip to the fourth bucket and not take a shot.

- PASSIVE: Once you've allocated to the 3 buckets above you can start deploying all other excess capital into owning assets that produce cash flow. You need equity and ownership of diverse assets to live on forever. These are things like owning real estate, owning equity in companies, etc. Many people make the mistake of diversifying far too early when they don't have a lot of money. This bucket is the appropriate time when diversification makes the most sense.

Once your cash flow (that's not directly tied to your time) exceeds your expenses, you're financially free.

The asymmetric risk bucket is different for everyone - it depends on your goals. You may skip it entirely and move to the last bucket right away. Or it may not work and you have to try multiple times here before moving past it.

If your asymmetric bet PAYS off early, you take risk off the table and can diversify into passive cash flow options.

If your asymmetric bet doesn't pay off, you are still set with retirement long-term and can try again depending on your goals and time horizon. If it's not worth your risk, you can move to the passive bucket and start building slowly.

Recap

This is how I think about and structure my own personal sequence of investing. Your own sequence will depend entirely on YOUR goals, time horizon, risk tolerance, and many other factors. I'm not saying this method above is correct, but hopefully, it will give you factors to consider when crafting your own and understanding how to manage risk.